If you do one thing today, look into investing your pension.

A ten minute task could completely change your financial future.

2/8/20243 min read

First and foremost this is not investment advice, we are a group of finance nerds who are interested in pensions, if you think you need advice always speak to a professional!

According to thisismoney 90 to 95% of people in the UK stick with their default pension fund.

We would imagine a lot of UK residents don't even realise they can change their default pension fund. Default funds are generally lower risk lifestyle funds.

This is fine for a lot of people and their risk preferences, but there are those amongst us that are more comfortable with risk and are happier to risk more for the potential of a greater return down the line.

The barrier to entry to see what you are invested in is often a quick check of your most recent pension statement, plugging a URL into google and setting up your online account. Depending on your pension provider there will be a range of different funds that your existing pot and future contributions can be allocated to.

Unsure of how to allocate your pension? You should seek financial advice - you may have a designated advisor through your workplace scheme and you can get their details from payroll or HR.

They will likely run you through an investment risk assessment - a fairly straightforward form with some questions on risk vs reward to gauge your risk appetite. A quick google for investment risk assessment will give you an example of these forms from different providers (i.e. Vanguard, Standard Life etc)

to give you a flavour of what is involved. (Forbes has quite a good article on this concept https://www.forbes.com/advisor/investing/investment-risk-tolerance-quiz/

This assessment will generally provide an indicative risk number that you can filter possible funds against.

What could changing your pension investment mean in terms of your future finances?

Take all of the below with a pinch of salt - investments can go up and down and the assumptions below are just that, assumptions.

The higher risk, higher reward fund user

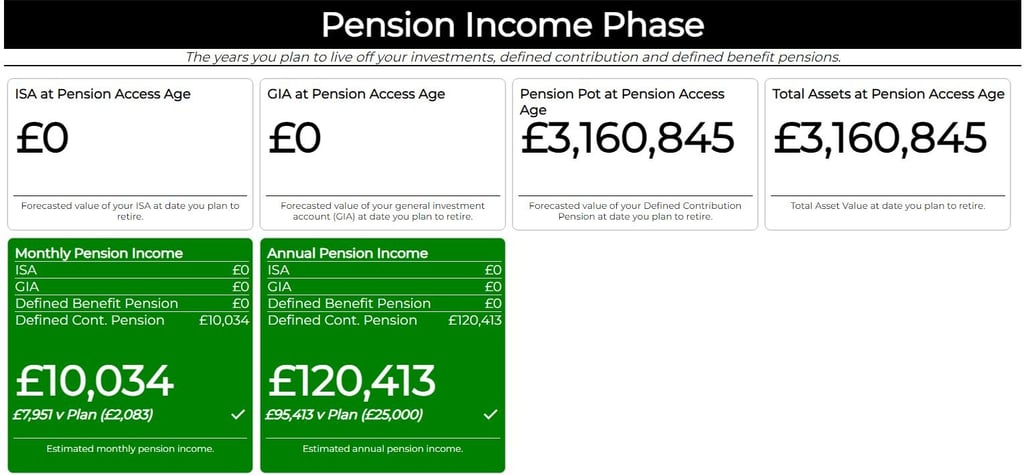

At 68 employee two smashes her income goal and has a significantly bigger pension pot of over £3Million.

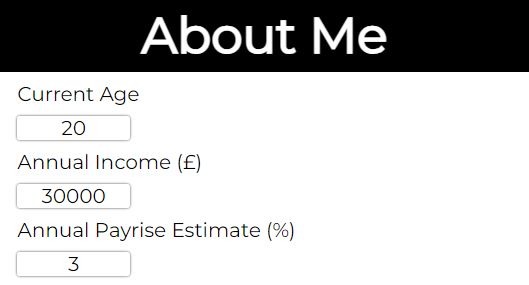

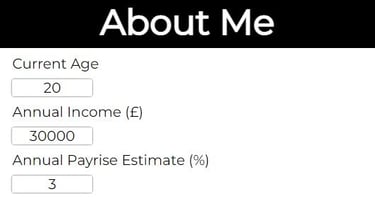

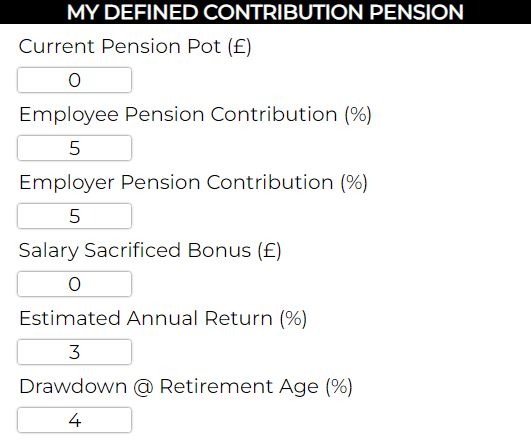

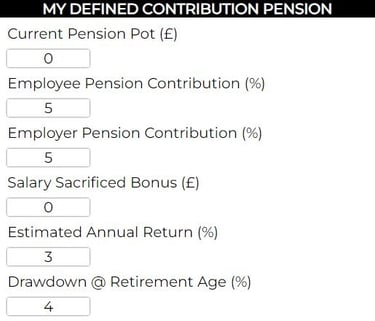

Two identical 20 years old with a defined contribution pension putting 5% towards your pension which is matched at 5% by their employer.

They earn 30k a year and expect to make roughly 3% more each year.

Both plan to retire at state pension age of 68

Employee One doesn't know he can change his pension and leaves it in a low risk low reward fund which gives him an annual return of 3%

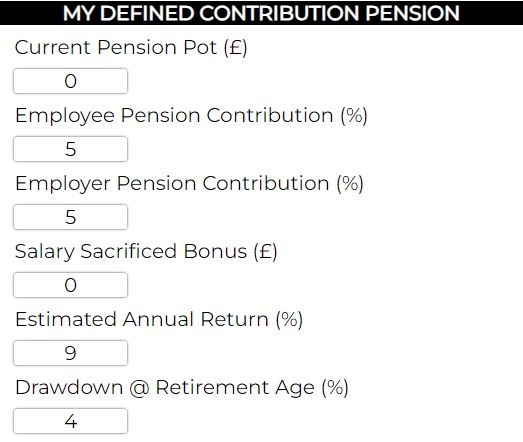

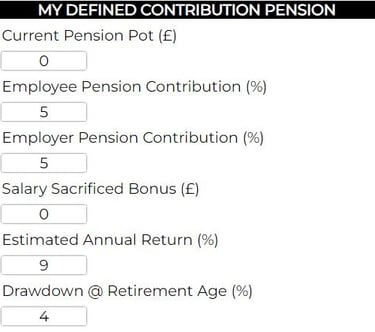

Employee Two decided she has is comfortable with a higher risk profile in return for a higher potential reward. She researches some funds and invests in a higher risk fund which gives her an annual return of 9%

Both have determined they need £25,000 a year and they both plan to drawdown 4% annually from their defined contribution pension.

(The following results ignore inflation and assumes return rate is post investment fees).

The default fund user

At 68 employee one doesn't quite meet his target income and has a pension pot value of £589,094